The CIR team has recently returned from the OFC trade show where much fuss was made about the opportunities for fiber optics in the 5G infrastructure and C-RAN. CIR has also just published a report on “C-RAN Deployment: Market Opportunity Analysis – 2018 and Beyond,” in which we also extol the revenue potential of the coming 5G “revolution.”

CIR believes that C-RAN opportunities are all ultimately related to the critical need to keep the cost of building 5G infrastructure as low as possible. One might say this about any large infrastructure project. But as we see it, 5G screams out for low costs (a) because mobile phone companies do not generate as much free cash as they once did (especially in Europe) and (b) because the new revenues that are supposed to flow from 5G are at best uncertain. And 5G that didn’t go beyond 4G LTE in terms of the number of service offerings would be a financial disaster.

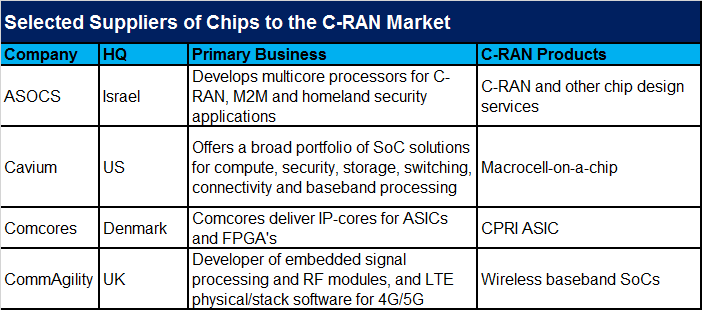

As CIR sees it, one of the sectors that benefits most from the rise of C-RAN are the specialist chipmakers – firms that fabricate FPGAs, SoCs, ASICs or specialized processors. Through embedding some of the critical C-RAN and related functionalities at the chip level, these chip makers can bring new value propositions to the 5G community. Already, there is a handful of firms that are specifically exploiting this opportunity (See Exhibit, below). CIR analysis suggests that the consumption of processors and other electronic components by the C-RAN market will be around $250 million reaching $500 million by 2023.

There is money to be made here. Yes, $500 million is a drop in the bucket compared with worldwide chip industry revenues –usually pegged in the hundreds of billions. But CIR sees 5G infrastructure as a significant new way for firms to profitably fabricate highly specialized chips over the coming decade. The focus on niches in this way is a long-established strategy in the semiconductor industry. The C-RAN niches that appear to CIR to offer the greatest opportunity for the semiconductor industry are processors specially designed for C-RAN, baseband components, CPRI components, macrocell components, and NFV and SDN components.

Source: CIR

CIR’s analysis of the strategies that the firms listed in the Exhibit are employing reveals some innovative market strategies, which we think are available not only other chip makers, but also to other firms seeking to make money from 5G infrastructure products.

Alliances with OEMs, but carriers also: Chip makers usually sell to OEMs. Nonetheless, we are seeing carriers that are deep enough into C-RAN technology development to work with chip makers directly. A case in point here is Cavium which has supplied its OCTEON Fusion macrocell-on-a-chip platform to power the 4G/LTE small cell deployment required for SK Telecom’s C-RAN roll-out in Korea. Cavium has also signed an agreement with China Unicom to accelerate the design and development of virtualized BBU and provide a path for 5G adoption. And it’s not just Cavium, ASOCS has signed a strategic memorandum of understanding with China Mobile for the joint development, commercialization, testing and deployment of large-scale baseband processing units for China Mobile’s C-RAN efforts.

While, there is not yet a proof that Cavium will succeed in its efforts, our takeaway here is that there may be a way that even chipmakers can embed themselves in the consciousness of important carriers, impressing OEMs and getting themselves designed in to the carriers’ future C-RAN/5G plans. There may be no half way houses to success with this strategy. We note that Cavium’s product is a complete L1-L7 implementation supporting base station designs that range from high capacity picocells at 800 simultaneous users all the way up to multi-sector macrocells with up to 3,600 simultaneous users. It may be than anything less than this would not win carrier support.

Off-the-shelf vs. proprietary chips: The conventional wisdom has it that the way to make money in specialized chips is with proprietary ASPs and at some level, this is certainly the case – this is why equipment makers often make their own ASPs. CIR anticipates that this will be a popular strategy in the C-RAN chip business, where, for example, eASIC is collaborating with ASOCS in the development of a custom silicon device for the acceleration of next-generation network virtualization applications utilizing the eASIC Nextreme-3 platform.

Nonetheless, as CIR sees things, a proprietary chips strategy is not without its risks – most importantly misjudgments about times to market and the possibility that a proprietary offering might underperform. Yet there is also another way.

Consider CommAgility, which develops, signal processing technology and RF modules for 4G/5G deployments has built this business using a hybrid approach that combines DSPs with standard processors including ARM architectures and TI chips. For example, CommAgility’s AMC-K2L-RF2, is billed as a low-cost, high performance ARM- and DSP-based processing card that can be used either as a complete baseband and RF small cell solution, or as a pure RRH with its CPRI interface linking to a separate BBU. The main processor is the TI TCI6630K2L SoC.

A future: On balance C-RAN chips should be considered a volume opportunity. But until 5G standards are in place (in a couple of years) and we start to see whether consumers stand up and salute the new broadband services promised by 5G, there will be many uncertainties about the revenue potential for C-RAN chips. CIR’s forecast numbers quoted at the beginning of this article are predicated on strong growth for C-RAN, but, of course, it things could turn out otherwise.

In the meantime, we are beginning to see a few specialized semiconductor firms begin to respond to the call of C-RAN. Whether the chip firms that we mention above will turn out to be the ones who make the most money out of C-RAN it is surely too early to say. On the other hand, we are getting the first glimpses of how firms in the chip industry are strategizing for the C-RAN opportunity.

Direct collaborations between chip companies and mobile operators seem one strategic possibility. And the design activity market is likely to remain divided among the risky (but potentially very profitable) DSP route and building value added on top of off-the-shelf chips.